What is a SIP (Systematic Investment Plan)?

What is a SIP (Systematic Investment Plan)?

SIP is not an investment—it’s a strategy.

It’s a method where you invest a fixed amount in a mutual fund at regular intervals (monthly, quarterly, or weekly).

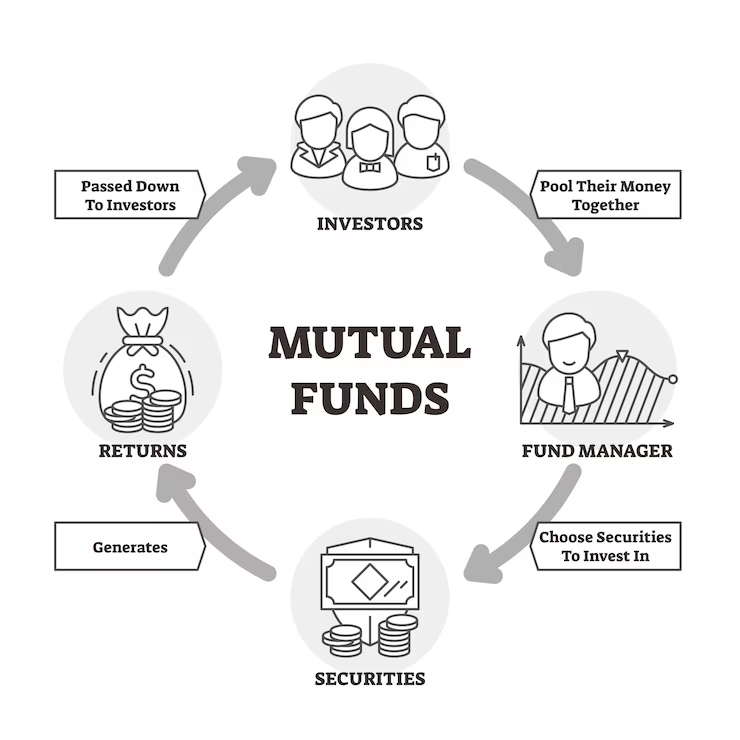

How SIP Works:

- You choose a mutual fund scheme.

- Select the investment frequency (e.g., ₹5,000/month).

- Money is automatically deducted from your bank and invested in the fund.

- Over time, you accumulate more units of the mutual fund.

Benefits of SIP:

Benefits of SIP:

Benefits of SIP: Rupee Cost Averaging: You buy more units when the price is low and fewer when it’s high → reduces overall cost per unit.

Rupee Cost Averaging: You buy more units when the price is low and fewer when it’s high → reduces overall cost per unit.

Disciplined Investing: Automates investing → no emotional decisions.

Power of Compounding: Long-term SIPs benefit from compounding growth.

Example:

Example:

You start a ₹5,000 monthly SIP in a mutual fund offering 12% annual returns. After 10 years, you’ll have invested ₹6 lakh, but your portfolio value will be around ₹11.6 lakh—thanks to compounding.

“Want tax benefits too? Check these ELSS funds.”

Which One Should You Choose?

Choose SIP If:

You’re a new investor with limited capital.

You’re a new investor with limited capital.

You want consistent, disciplined investing.

You’re aiming for long-term wealth creation.

You want to reduce market volatility risk.

Choose Lump Sum Mutual Fund Investment If:

You have a large sum to invest (bonus, inheritance, etc.).

You’re confident about market timing.

You want potential for higher short-term returns.

You can handle market fluctuations.

“SIP and mutual funds are core to any 2025 investment strategy.”

Conclusion: SIP or Mutual Fund? It Depends on Your Goals!

Conclusion: SIP or Mutual Fund? It Depends on Your Goals!

Conclusion: SIP or Mutual Fund? It Depends on Your Goals!Both SIP and lump sum mutual fund investments have their place.

My Recommendation:

- For consistent wealth creation, go for SIPs.

- For strategic short-term gains, opt for lump sum mutual funds.

Ready to invest? Start your SIP or mutual fund journey today and watch your wealth grow!

Ready to invest? Start your SIP or mutual fund journey today and watch your wealth grow!

Here are funds dominating this year